By Nick Buffie and Bob Lord

In recent months, reporting by ProPublica confirmed that some of the wealthiest billionaires in the United States are paying virtually no income tax on the incredible gains in their fortunes.1 Worse, a massive loophole in the tax code allows these billionaires and other wealthy Americans to escape income tax on their gains for their entire lifetimes—even as regular Americans pay income tax on every paycheck.

To pay for the transformative investments in his Build Back Better agenda, President Joe Biden has proposed tax reforms to close a capital gains loophole favoring the wealthiest Americans. This change is the most important way that Biden’s plan combats the tax code’s preferential treatment of income from wealth over income from work.

Under the American Families Plan (AFP), only a small fraction of Americans—those with very large untaxed gains—would be affected, mainly because the plan exempts the first $1 million of untaxed gains per person.2 And while critics of the president’s plan have argued that it would harm family farms and businesses, these claims are unfounded. As this issue brief explains, many of these claims are based on flawed studies, including some that do not even analyze the actual Biden proposal.

The fact is that under the AFP, the vast majority of Americans—including family farmers and small-business owners—would be exempt from new taxes, since the proposal is targeted at those with large untaxed gains. Moreover, the proposal includes special protections for owners of family farms and businesses who plan to keep their enterprises in the family. Because of these protections, critics’ harshest claim—that the Biden plan would force families to sell their farms and businesses, thereby preventing transfers from one generation to the next—is simply not true.

The AFP closes a loophole that allows huge fortunes to permanently escape income tax

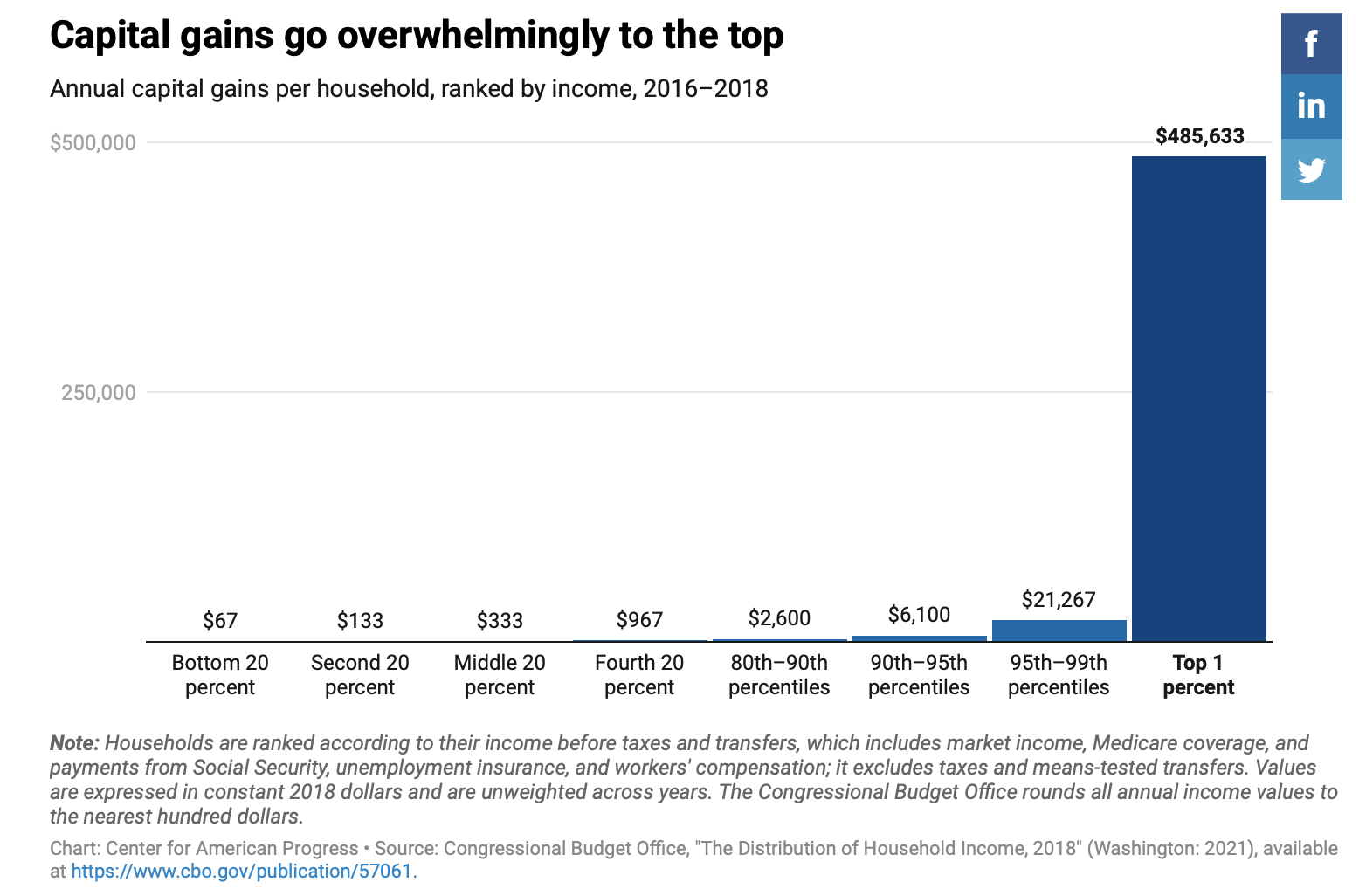

To support vital public investments, President Biden’s plan would raise $3.6 trillion in revenue from high-income Americans and corporations over the next decade, including nearly $350 billion from reforming the taxation of capital gains.3 Capital gains are the growth in the value of assets between when they are bought and when they are sold. Because of the extreme concentration of wealth in the United States, capital gains accrue overwhelmingly to the very rich. According to data from the Congressional Budget Office, households in the top 1 percent of the income distribution collect nearly $486,000 per year on average in realized capital gains; those in the bottom 20 percent make just $67.4 Central to President Biden’s tax reform is his proposal to repeal the stepped-up basis loophole—which shields these types of gains from income tax—while protecting the savings of ordinary Americans.

Figure 1

Stepped-up basis is one of multiple ways that capital gains receive favorable tax treatment. Under the existing tax code, gains on assets are generally not taxed until they are sold. If a wealthy person buys stock for $1 million and it rises in value to $11 million, they do not owe any tax as long as they hold the asset—even though they have become $10 million wealthier.5 If the person sells the asset, they would realize a $10 million gain and include that amount in their taxable income. Assuming the person has held the asset for more than one year, the gain would be taxed at the rates for long-term capital gains, which are significantly lower than those for other forms of income.6Though the asset value grew over years, the tax is deferred until sale and is subject to much lower rates when it is taxed. By contrast, income derived from labor—such as wages—is generally taxed as it is earned and is subject to ordinary rates.

Moreover, stepped-up basis allows gains on assets to permanently escape income tax if the owner never sells the asset during their lifetime. If an individual holds an asset until their death, the gain is simply erased at that time. No one—neither the decedent nor their heirs—pays any income tax on the gain accrued during the decedent’s life.

As the ProPublica reporting illustrates, the wealthiest billionaires in the country pay hardly any income tax from year to year because they often sell little to none of their stock holdings.7 This means that some of the largest fortunes in human history will permanently escape income tax if Congress fails to change the revenue code before these billionaires pass their fortunes to their heirs.8

Biden’s tax reforms only affect a tiny share of Americans

The AFP does not repeal the stepped-up basis loophole entirely. Under the plan, up to $1 million in untaxed gains per person—$2 million per couple—would still be exempt from taxation. This would come on top of other capital gains carveouts, including the exemption of $250,000 of gain on home sales—$500,000 for couples—and the exclusion of sales of qualified small-business stock.9

Unsurprisingly, very few people would be affected by these tax hikes. Robert McClelland of the Tax Policy Center estimates that a miniscule 3 percent of households have unrealized capital gains greater than $1 million per person.10

Above the exemption levels, President Biden’s plan would repeal stepped-up basis by counting gifts and bequests of appreciated assets as realization events, requiring the original owner to include the appreciation of the asset in their taxable income. In the case of a bequest, this would fall on a decedent’s final income tax return.11 Taxes on liquid assets such as stocks would be due that year, but taxes on nonliquid assets such as farms and businesses could be paid over 15 years.12

Moreover, the AFP allows heirs of family-owned farms and businesses to defer taxes indefinitely so long as the farms or businesses continue to be owned and operated by members of the family. Taxes are only owed on the original owner’s gain when the enterprise is sold or is no longer operated by the family.13 For this reason, no one inheriting and operating a family farm or business would be forced to sell it for the purpose of paying new taxes under the Biden plan.14

Critics of the AFP ignore its specific protections for family farms and businesses

President Biden’s proposals to tax the rich are overwhelmingly popular.15 Consequently, the president’s critics have been hesitant to attack his plan directly. For example, a recent CNBC profile of the business lobbying group America’s Job Creators for a Strong Recovery (ACJSR) noted the following:

The coalition [ACJSR] aims to turn the narrative away from a debate about taxing the rich and the biggest corporations to pay for roads and bridges. The organizers themselves acknowledge that that rhetorical battleground leans strongly in Democrats’ favor in public opinion polls.16

ACJSR has instead mischaracterized President Biden’s plan as a tax hike on families. Eric Hoplin, one of the group’s leaders, claimed that the Biden proposal would “enact record high taxes on America’s individually and family-owned businesses,” a phrase ACJSR has reiterated in multiple outlets.17

Other groups have similarly accused the AFP of harming family farmers.18 An article in the Northern Ag Network paraphrased Sen. Steve Daines (R-MT) as saying that the president’s plan would “destroy the generational handoff of farms and ranches.”19Daines also said that “[t]he only way Montana farmers and ranchers could get through this, would be to sell off part or even all of the family farm or ranch.”20 Daines’ quote implies that income tax would be due on family-owned farms or ranches when they are handed down to another generation. But that is not true, for two reasons. First, most family farm and ranch owners would fall well under the exemption thresholds in the AFP. And second, even those with more than $2 million of gain will be able to defer their income taxes indefinitely so long as their farm or business continues to be owned and operated by members of their family.21

Critics of the AFP cite misleading and flawed studies

To make these tenuous assertions appear valid, President Biden’s critics have cited two studies: one from the Agricultural and Food Policy Center (AFPC) at Texas A&M University and another from the accounting firm EY, formerly known as Ernst & Young.22Both studies dramatically overstate the impact on family farmers and business owners from repealing stepped-up basis, and neither directly examines the Biden plan. Nonetheless, the studies have gained attention because of the novelty of their conclusions, which greatly exceeds the strength of their evidence.

The AFPC study

On July 21, 2021, Sen. John Boozman (R-AR) claimed on the Senate floor that President Biden’s plan would “crush rural America.”23 He highlighted a study that Republicans on the Senate Committee on Agriculture, Nutrition, and Forestry and the House Committee on Agriculture had requested from the AFPC.24 Boozman asserted that if President Biden’s plan were implemented, 92 of the 94 “representative farms” selected by the AFPC “would be impacted with an average additional tax liability of more than $720,000 per farm.”25 In a similar vein, House Agriculture Committee Republicans cited the study to claim that if combined with a wholly separate bill, changes that “mirror” President Biden’s plan would cost those 92 farms an average of $1.4 million each.26 Finally, Sen. John Thune (R-SD) cited the AFPC study in a Fox News op-ed, writing:

But the Biden administration is targeting this longstanding part of the tax code [stepped-up basis] as it scrambles to pay for its far-left crusade to permanently grow the federal government and fund the massive tax breaks they’re proposing for wealthy Americans in blue states.

The Texas A&M Agricultural and Food Policy Center studied how this new tax would affect family operations, and it found that 98 percent of the representative farms in its 30-state database would pay a big price. How much? On average, the proposal would increase the tax liability by $726,104 per farm.

Nobody likes paying taxes, but this heavy additional burden – again, often on unrealized gains – has the potential to force families to sell off part of the farm or lose the farm entirely just to pay a tax bill.27

For starters, policymakers should recognize that the AFPC study does not consider President Biden’s plan. Rather, the study focuses on an estate and gift tax bill—the For the 99.5 Percent Act—introduced in Congress and another proposal—the Sensible Taxation and Equity Promotion (STEP) Act of 2021—put forward as a discussion draft.28

The For the 99.5 Percent Act, sponsored by Sen. Bernie Sanders (I-VT) and Rep. Jimmy Gomez (D-CA), would change the taxation of estates, gifts, and trusts in a number of ways, most notably by decreasing the exemption amount and introducing higher marginal rates for the estate tax.29 President Biden’s budget, however, currently includes no estate tax changes.30

Like the AFP, the STEP Act—sponsored by Sen. Chris Van Hollen (D-MD)—seeks to eliminate the stepped-up basis loophole. It also includes a $1 million exemption threshold—$2 million for couples—and allows new tax liabilities to be paid over 15 years.31 But unlike the president’s proposal, the draft of the STEP Act did not include specific protections for family farms and businesses. The reason that no protections are spelled out in the bill is precisely because it is a discussion draft, and its authors have invited outside input before introducing an actual bill.32 As noted above, President Biden’s plan guarantees that no taxes will be owed on family-operated farms and businesses until those farms or businesses are ultimately sold; this deferral of tax liability was not included in the STEP Act discussion draft studied by the AFPC.

More importantly, the AFPC study contains multiple methodological flaws. First, the AFPC’s selected farms are hardly “representative” of family farms nationwide. Although the word “representative” makes dozens of appearances in the AFPC report, there is little clarification as to who or what is being represented.33 At one point, the authors briefly note that “AFPC’s representative farms and ranches are all assumed to be full-time, commercial-scale family operations.”34

This means that the AFPC’s 94 farms are unrepresentative of family farms generally. According to 2019 data from the U.S. Department of Agriculture (USDA), just 8.2 percent of all family farmers own commercial farms. Moreover, these commercial farmers are far wealthier than the 91.8 percent of noncommercial farmers.35 This skews the AFPC study toward the very wealthiest family farmers.

Second, even after limiting itself to commercial farms, the study gives disproportionate weight to large commercial farms. The most recent AFPC study does not discuss the selection criteria for the farms, but in a March 2021 AFPC study of the same 94 farms, the researchers noted:

AFPC has developed and maintains data to simulate 94 representative crop farms, dairies, and livestock operations chosen from major production areas across the United States. … Often, two farms are developed in each region using separate panels of producers: one is representative of moderate size full-time farm operations, and the second panel usually represents farms two to three times larger.36

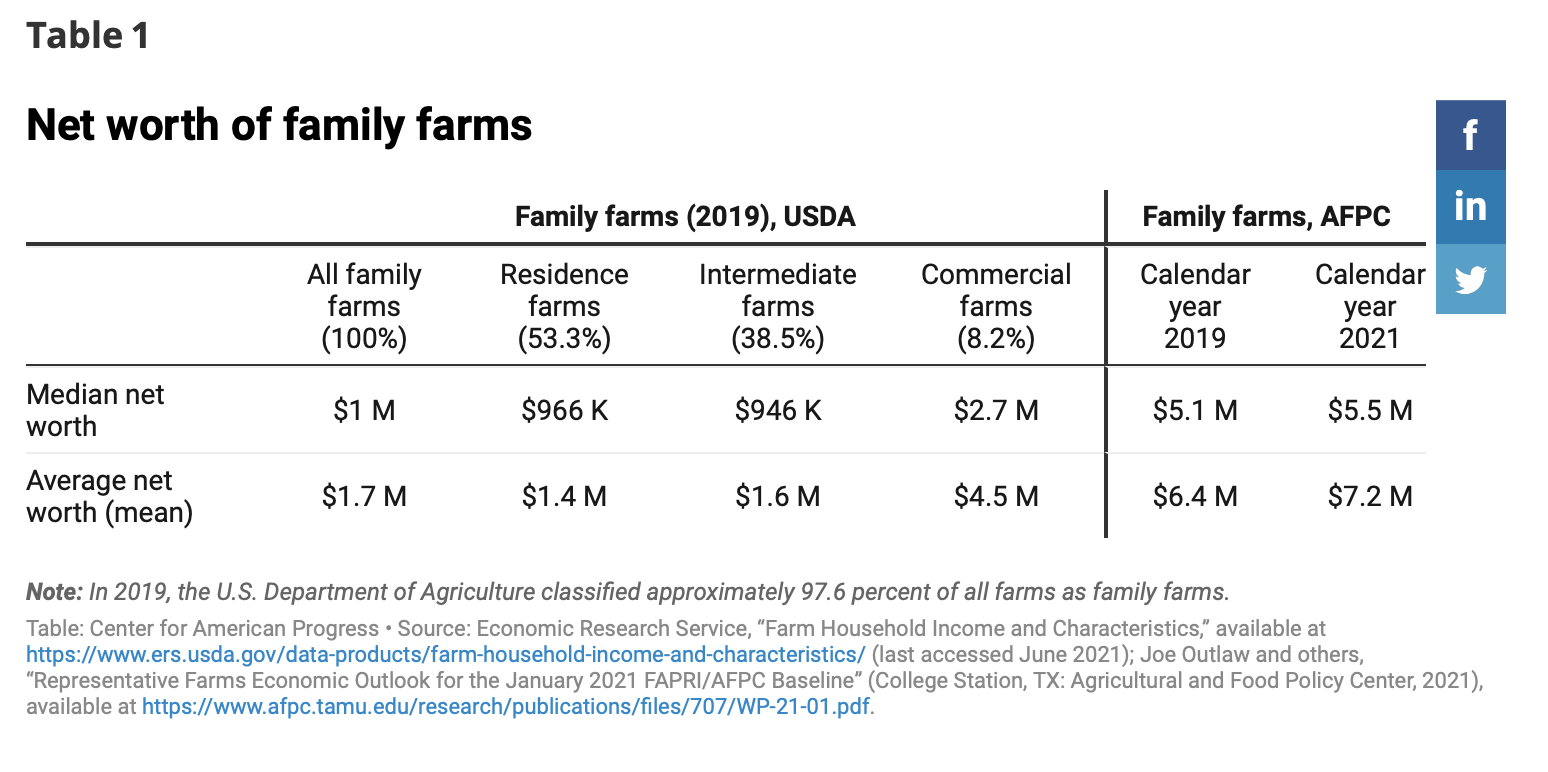

For AFPC farm households, median net worth was roughly five times the national median, and average net worth was nearly four times the national average.37 (see Table 1) This discrepancy cannot be explained away by confounding factors. For example, even if one were worried about the USDA’s inclusion of small residential farms in its sample, this would not explain the large differences in net worth between AFPC commercial family farms and the commercial family farms surveyed by the USDA.

Table 1

The AFPC study exaggerates the burden of taxes in other ways as well. For example, consider the center’s assessment of the For the 99.5 Percent Act. The AFPC study highlights the act’s “average” tax increase for “impacted” family farmers, and those modifiers create two distortions.38 First, by limiting its analysis to “impacted” farmers, the AFPC excludes all farmers who would pay zero estate taxes under the For the 99.5 Percent Act. Second, the use of an average greatly exaggerates the effect on most farmers. If 99 individuals each owed $1 in taxes and one person owed $99,901, it would be misleading to declare that the “average” person owed $1,000 in taxes. This problem arises in the AFPC study, where a large share of the estate tax burden is borne by a minority of extremely wealthy farmers.

The AFPC researchers determine that with the For the 99.5 Percent Act’s provisions in place, 41 of the 94 farms would pay the estate tax, with an “Average Additional Tax Liability Incurred for Farms Impacted” of just less than $2.2 million.39 Using data from their March 2021 paper, the AFPC’s results have been replicated for this issue brief.40The authors follow the AFPC methodology of ignoring the increased deduction for Section 2032A special use valuation—an estate tax break for farms.41 According to this replication, an estimated 39 farms would pay estate taxes under the For the 99.5 Percent Act, and the average liability per affected farm would be $2.5 million.

The authors’ results show just how distortionary the words “average” and “impacted” are. The average estate tax for the 39 affected farms is $2.5 million, yet the average for all 94 farms is $1 million—just 41 percent as much. Moreover, the vast majority of the average tax would be paid by a small group of farmers. Fifty-five farmers would owe no estate taxes; 27 farmers would owe below-average amounts; and just 12 would pay more than the average per affected farm.42 These 12 estates—12.8 percent of farms in the survey—would be responsible for 65.8 percent of the total tax bill. And again, as noted above, these farms come from a sample that cherry-picks extremely large commercial farms.

Although the AFPC researchers published the net worth of all 94 farms in their March 2021 report, they have not made similar statistics available for each farm’s unrealized capital gains. If their data for unrealized capital gains are as dominated by a few rich farms as their data for estate values, then most of the STEP Act’s average burden will be borne by a small subset of AFPC farmers.

Finally, the AFPC study overstates the STEP Act’s impact on farmers by assuming that none of them are married, even though nationwide, roughly 4 in 5 farmers have a spouse.43 That is important because the exemption for unrealized capital gains is $2 million per couple but only $1 million for single individuals. In assessing the impacts of the STEP Act, the AFPC researchers assume that the farms in their study would be allowed to use the stepped-up basis provision for just $1 million, effectively underestimating the true step-up threshold by 50 percent.44

The EY study

Opponents of the AFP have also cited a study by the accounting firm EY. As with the AFPC study, the EY study has been used to attack the Biden plan even though it never comments on the president’s proposal.45

The EY study has two component parts. In the first part, the researchers give examples of how five hypothetical family businesses would be harmed by taxation at the time of the owner’s death. With business resale values averaging $74 million and ranging from $20 million to $200 million, EY’s hypothetical businesses do not remotely resemble typical family businesses in the real world.46

In the second part of their study, the researchers translate their hypothetical stories to real-world data. In that section, EY concludes that the economic cost of taxing capital gains at death would be just 0.04 percent of gross domestic product (GDP). Moreover, just one-third of the cost would be borne by labor.47

As insignificant as that would be, it overstates the cost of the Biden plan for two reasons. First, the EY study—like the AFPC study—is not an assessment of the Biden plan. Rather, it looks at the effects of immediate taxation upon the death of a business owner. As such, the EY researchers do not account for how tax deferral would protect family businesses, nor do they account for the Biden plan’s exemption of $2 million per couple. When the EY researchers analyze a second proposal more akin to true tax deferral, they find that the total economic cost would be just 0.02 percent of GDP—exactly half of an already small number.48 Critics who cite the EY study should be more forthright in noting both this point and that the $2 million exemption preserves stepped-up basis for the great majority of family farmers and business owners.49

Second, EY’s analysis fails to account for the economic benefits of eliminating the lock-in effect associated with stepped-up basis.50 With stepped-up basis, investors and business owners have an incentive to hold assets until their deaths even if they otherwise would have sold the assets. This harms economic efficiency and growth.51Repealing stepped-up basis would make capital more liquid since there would be less incentive to hold assets indefinitely.

Extrapolating from the conclusions reached in the EY study, the macroeconomic cost of the Biden plan would be somewhere between trivial and nonexistent. Meanwhile, the $350 billion in revenue from reforming capital gains taxes would be invested in ways that enhance growth and support working families. The EY study also fails to analyze President Biden’s proposals on the spending side. Instead, it merely includes assumptions about generic government spending.52

The AFP taxes the rich, not working-class families

While there would be no additional taxes under the Biden plan for farms and businesses that remain family-owned and -operated, taxes would go up substantially for wealthy individuals who are only passive business owners.

Consider family farms. The word “operated” ensures that tax deferral will only extend to actual farmers—not to wealthy individuals who happen to own farmland. According to 2014 data from the USDA, 31.1 percent of the country’s farmland is owned by nonoperating landlords—people who rent out the land but do not farm it themselves.53For example, before their recent divorce, Bill and Melinda Gates owned more farmland than any other couple in the country.54 Because the Gateses do not operate their own farmland, they would not qualify for tax deferral under the Biden plan.

Moreover, the Gateses and their heirs are not an exception to the rule. Of the 283 million acres of farmland currently owned by nonoperating landlords, 53.8 percent were either inherited or gifted.55 Had the Biden plan been in place when these nonfarmers inherited their land, they would have paid taxes on unrealized capital gains above the $2 million threshold.

The AFP protects genuine family farmers even as it taxes wealthy landlords. According to the USDA, 98 percent of family-owned and -operated farm estates would not incur any additional taxes when parents’ assets are passed to their heirs.56 Under the Biden plan, such families would have their tax payments deferred so long as the farm remained in the family. The remaining 2 percent would pay higher taxes only on their nonfarm assets. For example, even if Bill Gates were to begin farming his own land and could thus take advantage of the Biden exemption for family-operated farms, he would still have to pay taxes on the gains from his Microsoft stock and any other nonfarm assets he owned.57

Conclusion

Under the AFP, working-class parents could pass their farms and businesses to their children without having to pay any capital gains taxes at the point of transfer. Yet proponents of the tax code status quo are hiding behind family farmers and business owners to protect a far different group: the extremely rich.

Middle-class Americans generally do not have significant capital gains. Households in the middle fifth of the income distribution realize just $333 in capital gains each year.58If they accrue similar amounts of unrealized gains, it would take more than 6,000 years to surpass the American Families Plan’s $2 million exemption threshold. Although life expectancy is projected to rise in the future, it is unlikely that the Biden plan will raise taxes for ordinary working people.

Families who work their own land or operate their own businesses will receive similar treatment. Typical family farms are not worth $7.2 million, and normal family businesses are not worth $74 million. The studies reporting enormous tax hikes for family farms and businesses cherry-pick their examples from a few exceptionally wealthy estates—because that is who will pay taxes under the Biden plan.

Those affected by the Biden proposal will not be family farmers or family business owners, but rather the heirs of stockholders, bondholders, and landlords. The working class will be protected, even as the passive rich will not.

Nick Buffie is a policy analyst specializing in federal fiscal policy on the Economic Policy team at the Center for American Progress. Bob Lord is an associate fellow at the Institute for Policy Studies and tax counsel for Americans for Tax Fairness.